A Guide to the Foundation of Net Zero!

In the domain of corporate climate accountability, greenhouse gas (GHG) emissions are categorized into three distinct scopes as per the Greenhouse Gas Protocol, the globally recognized standard for carbon accounting. Among these, Scope 1 emissions serve as the cornerstone of any net zero strategy due to their direct attribution to the reporting organization.

Scope 1 encompasses direct GHG emissions from sources that are owned or operationally controlled by the company. These are the emissions that arise as a direct result of the organization’s activities—emissions over which it has both operational command and data accessibility. Addressing Scope 1 emissions is therefore not only a compliance measure but a strategic imperative in any scientifically grounded decarbonization pathway.

Defining Scope 1 Emissions

Scope 1 emissions include all direct emissions from owned or controlled sources. This definition is rooted in the operational boundary approach, where an entity is accountable for emissions from equipment, infrastructure, or assets under its direct management. The emissions quantified under Scope 1 include but are not limited to fuel combustion in stationary and mobile equipment, fugitive emissions from refrigerants or pressurized systems, and process emissions generated from industrial or chemical reactions. The gases typically covered under Scope 1 include carbon dioxide (CO₂), methane (CH₄), nitrous oxide (N₂O), and fluorinated gases, each converted into CO₂-equivalent units using global warming potentials (GWPs) as defined by the IPCC.

What Falls Under Scope 1?

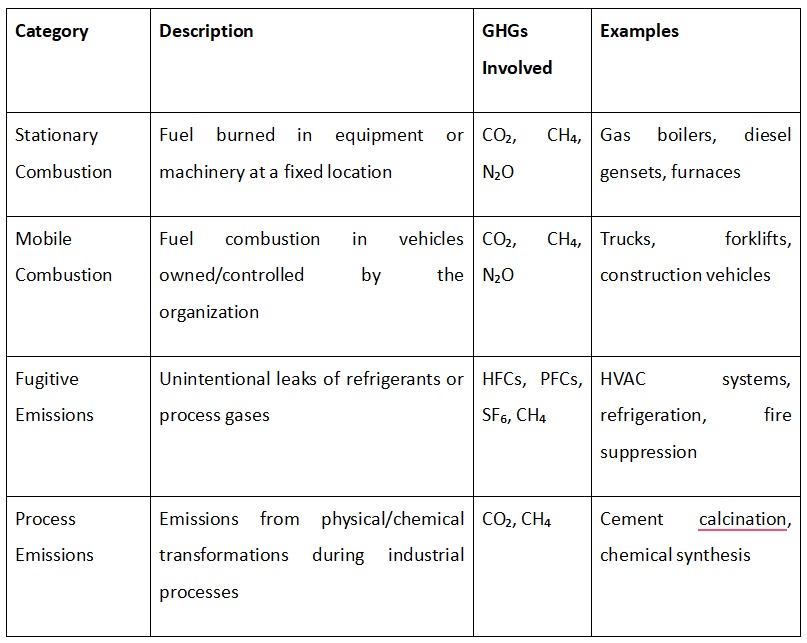

Scope 1 emissions originate from four primary categories, all of which involve direct physical emissions into the atmosphere:

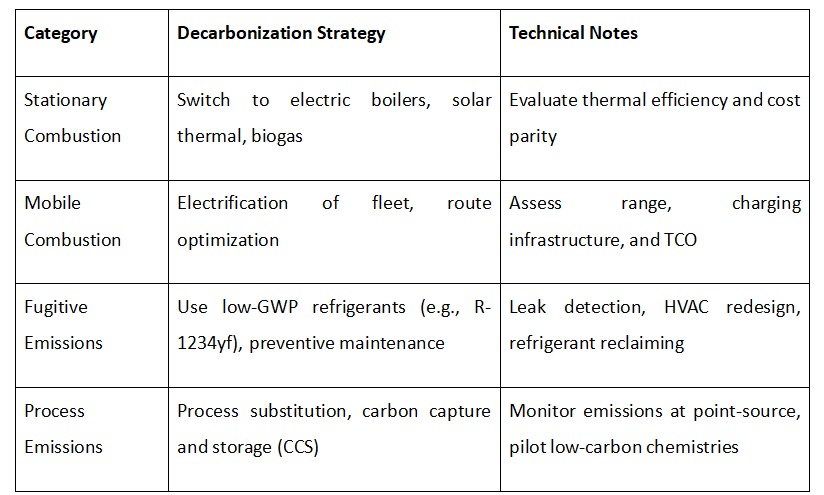

1. Stationary Combustion

This category refers to emissions from fuel burned in fixed assets such as boilers, furnaces, turbines, and generators. These assets are typically deployed in manufacturing plants, office buildings, or remote construction sites. For instance, a company operating natural gas boilers for heating in a regional office would record the combustion-related CO₂ and CH₄ emissions under Scope 1. The calculation is based on the volume of fuel consumed, corrected for calorific value and emission factor.

2. Mobile Combustion

This includes emissions from fuel use in company-owned or controlled vehicles such as delivery trucks, corporate fleets, construction equipment, and even forklifts. These emissions are often underestimated in companies with logistics or operations-heavy profiles. For example, diesel-powered trucks in a beverage distribution company will emit CO₂, N₂O, and CH₄, which must be accounted for based on distance traveled and fuel consumption data.

3. Fugitive Emissions

Fugitive emissions stem from the unintentional release of GHGs during the operation of pressurized systems, typically HVAC units, refrigeration equipment, or industrial gas systems. Hydrofluorocarbons (HFCs) and perfluorocarbons (PFCs) used as refrigerants have GWPs ranging from hundreds to tens of thousands, making even minor leaks significantly impactful. For example, R-410A, a common refrigerant, has a GWP of 2,088; a leak of just 5 kg would equate to over 10 tonnes of CO₂e emissions.

4. Process Emissions

Process emissions are generated from chemical or physical transformations intrinsic to industrial operations. These emissions are particularly relevant in the cement, steel, aluminum, and chemicals sectors. An example is the calcination process in cement manufacturing, where limestone (CaCO₃) is converted into lime (CaO), releasing CO₂ in the process. These emissions are structurally embedded in the production process and require substitution or capture technologies for mitigation.

Each of these categories must be accounted for independently using activity data and appropriate emission factors.

Calculation Methodology

Quantifying Scope 1 emissions involves activity-based data multiplied by emission factors. The basic equation follows:

Emissions (kg CO₂e) = Activity Data × Emission Factor × Global Warming Potential (if non-CO₂)

Activity data may include fuel quantities (liters or cubic meters), distance traveled, or weight of chemicals processed. Emission factors are regionally specific and should be sourced from authoritative datasets such as:

- IPCC 2006 Guidelines

- DEFRA (UK Department for Environment, Food & Rural Affairs)

- US EPA’s Emissions Factors Hub

- National GHG Inventories or Local Regulatory Bodies (e.g., SECR in the UK, MOCCAE in UAE)

It is critical that data collection be granular (preferably meter- or sensor-based) and auditable. For organizations pursuing external ESG assurance or sustainability-linked financing, the data quality, traceability, and frequency of measurement are paramount.

Example Calculations

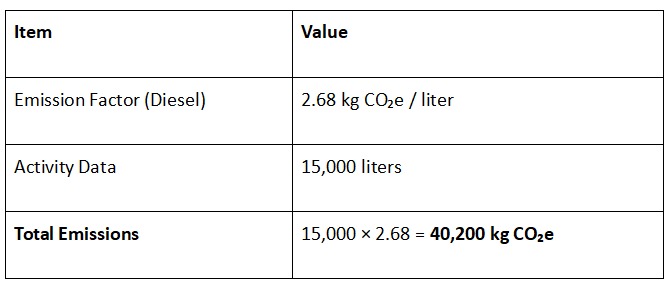

Mobile Combustion – Diesel Use in Fleet

A company-owned fleet consumed 15,000 liters of diesel last year.

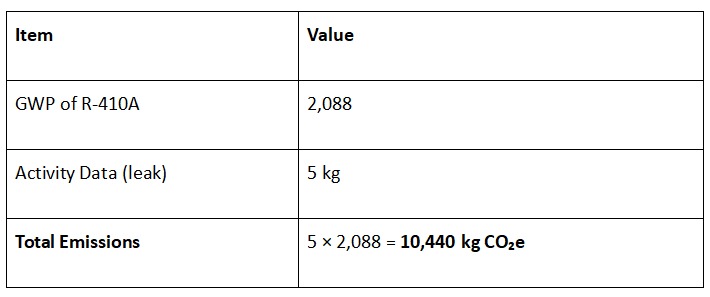

Fugitive Emissions – Refrigerant Leak

5 kg of R-410A refrigerant leaked from a cooling system.

Reduction Strategies by Category

Integrating Scope 1 into a Net Zero Strategy

A net zero roadmap must begin with establishing a robust Scope 1 emissions baseline, typically using the most recent 12-month period with reliable data. This baseline serves as a reference against which all future emissions reductions are measured. The organization should then define science-based targets (SBTs) in alignment with frameworks such as the SBTi Corporate Net-Zero Standard, which often requires absolute emissions reductions across all scopes.

The decarbonization of Scope 1 emissions typically involves three core levers:

- Fuel Substitution: Transitioning from high-carbon fuels like diesel and coal to lower-carbon alternatives or electrified processes.

- Technology Upgrades: Replacing legacy machinery with energy-efficient or zero-emission systems (e.g., electrification of fleets).

- Process Redesign and Capture: Redesigning operations to reduce process emissions or deploying carbon capture, utilization, and storage (CCUS) technologies.

Reduction interventions must be prioritized before offsetting. Offsets, where necessary, should be high-quality, verified, and represent carbon removals rather than avoided emissions.

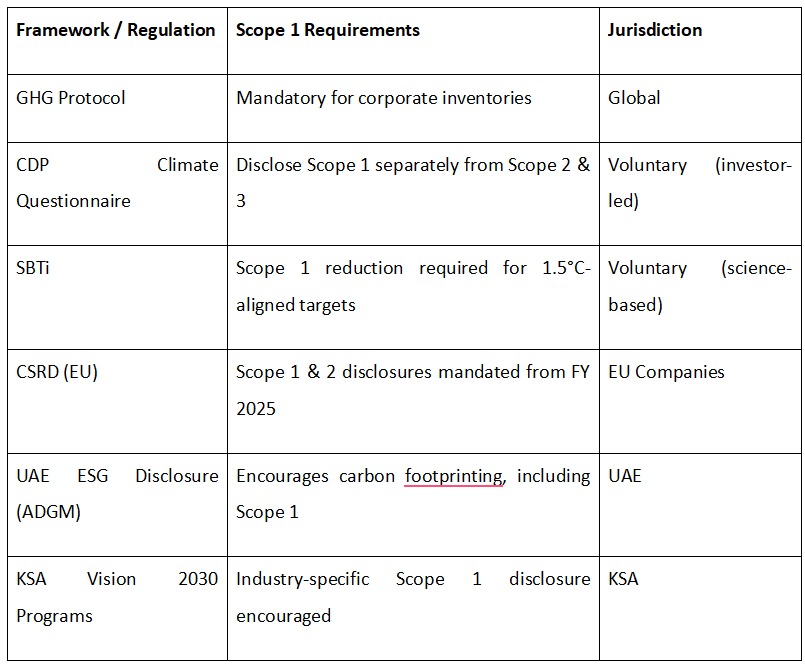

Regulatory and Disclosure Requirements

Globally, Scope 1 reporting is increasingly being mandated under both voluntary and compulsory disclosure regimes. For instance:

- The Task Force on Climate-related Financial Disclosures (TCFD) requires companies to disclose direct emissions as part of climate risk reporting.

- The Corporate Sustainability Reporting Directive (CSRD) in the EU enforces mandatory Scope 1 disclosures starting 2025.

- In the UAE and KSA, government-linked companies and large industrial emitters are being encouraged to align with national net zero strategies, requiring reporting under frameworks such as ADGM ESG Disclosure Guidelines or Vision 2030-linked GHG registries.

Furthermore, investor-driven platforms such as CDP (Carbon Disclosure Project) score companies based on emissions transparency, with Scope 1 forming the baseline metric of emissions intensity.

Common Misconceptions and Challenges

A frequent error in carbon accounting is the misclassification of emissions across scopes. For example, emissions from backup diesel generators may be mistakenly attributed to Scope 2 or left unreported entirely. Another challenge lies in overlooking low-volume yet high-GWP refrigerants—while their mass is small, their climate impact is disproportionately large.

Data granularity and system integration also present technical challenges. Many organizations lack integrated energy management systems (EMS) or asset-level monitoring infrastructure, which can lead to underreporting or estimation-based disclosures. The implementation of IoT-based metering and digital MRV (monitoring, reporting, verification) systems is now considered a best practice in operational emissions tracking.

Conclusion

Scope 1 emissions constitute the most controllable and accountable category of a company’s GHG footprint. Their effective management not only reflects operational excellence but also demonstrates leadership in climate governance. A technically sound understanding of the sources, quantification methods, mitigation strategies, and disclosure obligations related to Scope 1 is essential for any business committed to a credible net zero journey.

By addressing Scope 1 with precision and urgency, organizations can establish a strong foundation for deeper climate action—extending into Scope 2 procurement choices and Scope 3 value chain collaboration. As regulators, investors, and society intensify scrutiny, the path forward must begin with what is already within your control.

Start with your own operations. Measure accurately. Reduce systematically. Disclose transparently. That is the essence of Scope 1 stewardship.

About ESG Nexus

ESG Nexus is Pakistan’s premier sustainability consortium—bringing together SECP-registered ESG advisory and consulting leaders under one collaborative platform. We enable organizations to navigate regulatory complexity, embed ESG strategy, and accelerate their transition to a sustainable, net-zero future.